Very brief blog post this month; I'm deep into book writing mode at the moment. Chanelling Clif Assness, I'm just going to present a few charts and lead you to draw your own conclusions.

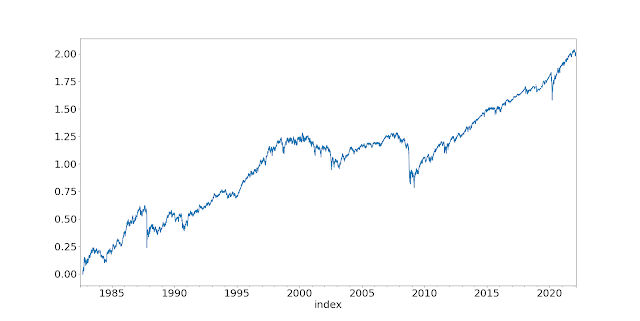

Excess / futures returns from portfolio of 60% S&P 500, 40% US Ten year treasuries (Authors own data)

Jorda et al “The rate of return on everything” QJE 2019

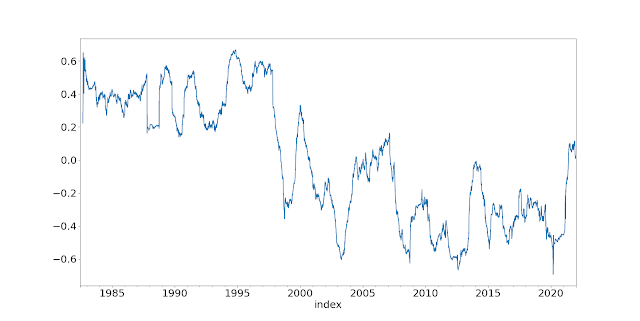

One year rolling correlation of S&P 500 and US 10 year bond daily % returns (Source; Authors own data)

|

| US inflation rate https://tradingeconomics.com/ |

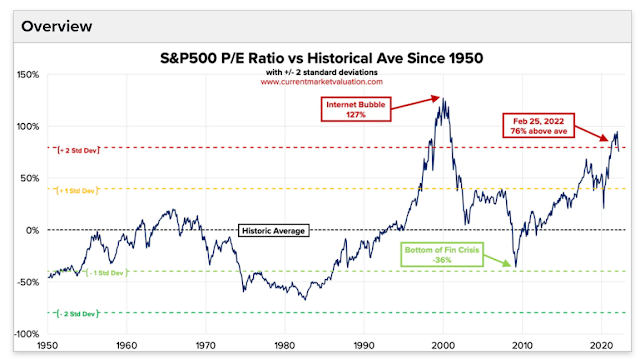

Source: https://www.currentmarketvaluation.com/

US 10 year interes rates. Source: tradingeconomics.com

And finally, for those who didn't get the Monty Python reference:

Footnote: The computing language, python, in which my trading system is written was named after Monty Python not the snake. Hence a certain publishing company that likes putting animmals on the front of their IT reference books might consider replacing the snake with a parrot...

Hi Rob,

ReplyDeleteThank you very much for all the information you give us. I heard about you from Andreas Clenow and now you are my favorite writer (sorry Andreas ...) although unfortunately, I do not have the background to understand everything you say.

I wanted to ask you the following:

1) regarding individual equities, is it better a momentum strategy or a trend following strategy (by choosing, for example, the stocks with the bigger capitalization per industry) to be followed?

2) by choosing different stocks (same asset class) and different trading rules it is possible a SR = 0.4 to be achieved, does that mean that someone must choose stocks which belong either to mid or small-cap index (annual st. dev. of returns bigger than 35%) so an account risk target of 20% can be achieved?

3) regarding stocks, would you go short as in futures?

4) in some brokers, the short side is much more expensive than the long side (in one case you buy the asset in the other CFD), for example, if the long side costs 0.01SR and the short side 0.15SR would you take the average 0.08SR and you would traded the instrument on both sides or would you went only long?

Thank you very much.

Keep doing what you are doing, your books are gold for the retail investor/trader.

Sorry for my English ... I am not a native speaker.

1) What's the difference between momentum and trend following? Aren't they just different words for the same thing?

Delete2) Not sure I completely understand your question, but if you have a diversified portfolio of blue chip stocks it's unlikely you will be able to consistently hit a risk target of 20% plus without leverage.

3) Sure I'd go short if I could and it wasn't too expensive (see next option), as you always get a boost from the short side

4) I wouldn't personally go short if it was going to cost 0.15 SR as that would wipe out any benefits

Hi,

DeleteFirst of all, thank you very much for your time.

1). I read this paper " Trend following, risk parity and momentum in commodity futures", Clare et al., 2014 (https://doi.org/10.1016/j.irfa.2013.10.001) (or I was trying to read it... I have not studied economics) and if I understand correctly momentum strategies are performance based (buy winners and sell losers) while trend-following strategies are rules based (e.g. moving averages crossover) and most importantly there is a difference in their skewness.

2). If I do not want / cannot use leverage the only way to have 20% account risk is to choose equities from small cap indexes of developed counties or equities from emerging countries. These stocks have 40% or bigger instrument risk (=annual standard deviation), so 40% divided by IDM= 2 (different instruments and trading rules), the account risk will be 20%. Am I wrong?

3. I have understood that you go short mainly to improve skewness and not for profit. So if someone does not use leverage and trades only stocks (negative skewness) there is no gain to apply a trend following strategy (positive skewness) in the short side. In other words, you improve the skewness of your returns but you lose money shorting stocks (for commodities, you make a small profit).

Thanks a lot again!

Ioan.

You haven't read the paper properly.

DeleteAccording to the authors "Momentum strategies involve ranking assets based on their past return (often the previous twelve months) and then buying the winners and selling the losers." Whilst "Trend following...

Trading signals can be generated by a variety of methods such as moving average crossovers and breakout"

So both are rules based. But momentum as defined by the authors is cross sectional whilst trend following is directional.

Personally I don't use these terms like this, hence my confusion.

I haven't researched trend following or 'momentum' on individual equities, but Andreas latest book describes a strategy that combines these. Incidentally, I discuss both strategies for futures in my new book, which I'm writing now.

2. Your calculation is correct.

3. No going short also improves profit

Τhanks for the help.

DeleteI have bought your published books and I will buy the new one too.

So the conclusion is: during high inflation periods stocks and bonds become correlated. Hence, diversification is diminished. Which means holding 60/40 will make for lots of financial suffering during high inflation / staglflation periods.

ReplyDelete